Uh-oh, Bitcoin, we have a problem.

2026-07-12

If you read the Bitcoin white paper [1], it presents the idea of a secure, peer-to-peer, decentralized digital currency, free from the shackles of modern bureaucracy & all of its inefficiencies. And the disciples of this utopian technology, like Brian Armstrong, tout it as a way of “increasing economic freedom” across the globe [2] (while simultaneously offering 50x leverage perpetual futures to American teenagers [3] to make to up for decreasing Q3 trading volume [4]).

But, does it really feel like that anymore? To me, it feels closer to 2008, where the institutional backing behind Bitcoin makes it “too big to fail”. Today, centralized exchanges handle ~86-90% of BTC volume [5]. And 40% of miners, which are the backbone of the network, are operated by publicly listed companies [6]. It doesn’t feel so peer-to-peer to me anymore.

Worse yet, the unit economics of mining bitcoin in the United States look bleak. With the surge in demand for AI inference, every Watt of power is a scarce resource that the capitalist machine needs to fight over. Theres a finite amount of power in the United States and it’s shifting away from Bitcoin and towards GPUs. In the last couple of months, how many times have you seen the headline: “US-based Crypto Mining Company XYZ has secured a deal with <Insert Hyperscaler> to repurpose their data center for High Performance Computing”. It’s become a trope at this point, but it’s a leading indicator of why cryptocurrency infrastructure is at a delicate point in time.

In this essay, we compare the unit economics of mining Bitcoin with serving AI inference, outline the seemingly inevitable migration of mining to emerging markets, and identify the companies positioned to benefit. Finally, we consider a strange but non-negligible possibility: that the United States subsidizes miners to keep the infrastructure securing its strategic reserve on American soil.

Show me the incentives

There’s few things that I believe in more than Charlie Munger’s famed quote: “Show me the incentives and I’ll show you the outcome” [7]. If I told a Meta software engineer that they could make $500K selling lemonade, I have a peculiar feeling that they would be on the corner of Broadway & Canal come Monday. So, to understand where Bitcoin mining goes next, we have to start with the incentives: what a megawatt earns today, what it could earn serving AI instead, and who captures the value when it moves.

As of July 12, 2026, the price of Bitcoin is roughly $64,129 [8]. Here’s what CoinShares estimates it currently costs top miners to mine it [9].

In the last 12 months, the following companies have begun complete transformations, working with hyperscalers to shift their data centers away from mining and towards AI inference [10][11][12][13][14]. Fun fact: In Q1 of 2026, the Bitcoin network’s hashrate dropped 4%, the first quarterly drop in 6 years [6]. CoinDesk explicitly tied it to miners pivoting to AI [6].

Cost per MW

Here is the nomenclature that you need to get familiar with and we’ll use throughout the remainder of the essay:

Watt (W): The rate at which an entity draws energy. For example, a light bulb utilizes 10W while a blow dryer needs 1500W. Watt is a way to measure Power [15].

Watt-Hours (Wh): The energy used when one watt is drawn for one hour. A 10W bulb running for an hour consumes 10Wh [15].

Watt-hour measures Energy (the amount), versus the Watt measures Power (the rate) [15].

Kilowatt (kW): 1,000 Watts. For example, an average household draws 1kW on average [15][16]

Megawatt (MW): 1,000,000 Watts. A single data center or bitcoin mining facility runs in the tens or hundreds of MW. This is the unit of measure that’s most useful to us.

Gigawatt (GW): 1B Watts. A large nuclear reactor draws ~1GW and the entire Bitcoin network draws ~20GW [15][17][18]

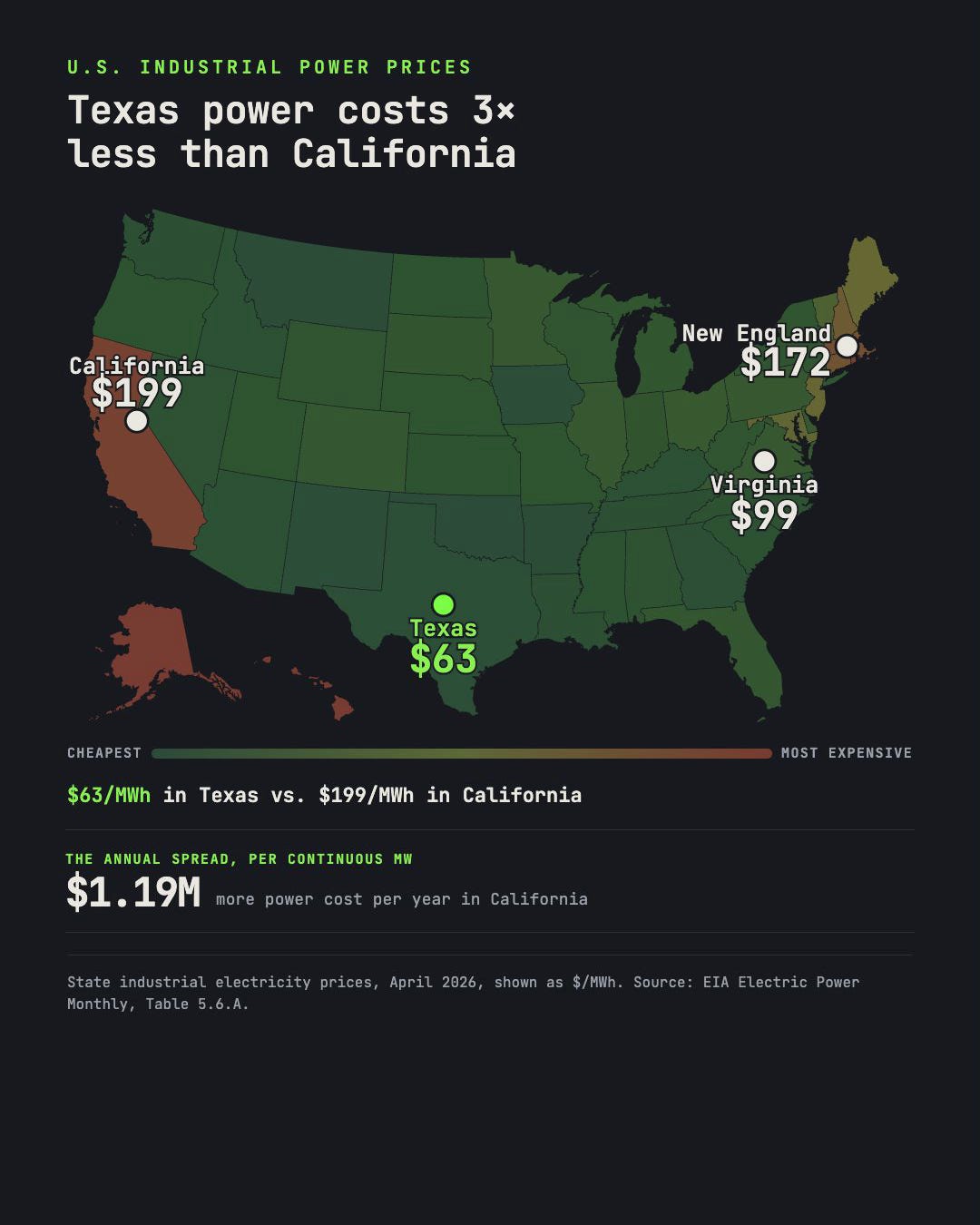

The cost of a Megawatt-hour is not the same across the continental United States [19]. It’s not a coincidence that the largest Bitcoin mining facility in North America is Riot’s 700MW facility in Rockdale, Texas [20].

Becoming a hash-slinging slasher

A mining hash is one double-SHA-256 (SHA-256d) calculation over a block header, whose Merkle root commits the block’s transactions [1][21]. Mining is nothing more than computing these values over and over again, trillions of times per second, hunting for the one hash whose output falls below a target value set by the network [21]. Whoever finds the first valid output “earns” the block subsidy, which currently pays out 3.125BTC, plus transaction fees [22]. This is a random process, so the best way to increase your chances of finding the right output is to increase the # of guesses [1][21]. This is often referred to as the hashrate [21]. One TH/s = 1 Trillion Hashes per second and a modern bitcoin-mining ASIC can typically generate 100-500 TH/s [21][23].

So, how much Bitcoin can you mine with 1 megawatt-hour?

I apologize for the math ahead of time. You can either follow along or jump ahead (it won’t hurt my feelings), but it wouldn’t feel right if I didn’t outline it.

One of the best ASIC chips on the market is Bitdeer’s SEALMINER A4, which does 886 TH/s on 8373 Watts, which translates to roughly 9.5J/TH [23]. But, that is a frontier ASIC, not the average machine operating across the network. The Cambridge Centre for Alternative Finance estimated a blended fleet efficiency of 28.2 J/TH in 2024 [18]. To account for subsequent hardware improvements, we use ~20 J/TH as our current blended-fleet assumption.

Over an entire day, the Bitcoin network grinds through 8.6 x 10e25 hashes (1ZH/s x 86,400 seconds per day)

The network produces an average of 450 BTC in block subsidies per day (3.125 BTC approximately every 10 minutes)

So, 1 Bitcoin ~ 1.9 x 10e23 hashes

One MWh = 3.6 x 10e9 Joules & that amount of energy buys you 1.8 x 10e20 hashes

Therefore, 1MWh represents 0.0009375BTC, which is $61, assuming the price of BTC is $65,000 [18][22].

Using statewide industrial electricity averages, if you mine that in Texas, it will cost you $63 in electricity, resulting in a loss of $2. If you mine that in California, it will cost you $199, a loss of $138 [19]. Running continuously for a year, one megawatt generates ~$534,000 of topline revenue [8][18][22].

Note: This doesn’t include land, staff, and other operating costs, which is why the cumulative costs to mine a Bitcoin are significantly more than just the cost of energy. See the first graphic above.

Follow the Money

Now that we’ve established the rough economics of mining Bitcoin, let’s look at the economics behind inference. At the moment, there are two main business models that miners are shifting to [10][11][12][24]. While both of them rely on taking GPUs and plugging them into the existing power infrastructure, the main question to ask is:

Who owns the GPUs?

Colocation

In a colocation arrangement, the Bitcoin miner supplies the scarce physical infrastructure: land, a grid interconnection, substations, transformers, a building, cooling, networking, and an agreed amount of energy capacity [24]. The tenant, usually a hyperscaler or a neocloud, supplies the GPUs and is responsible for operating them [24]. The miner is not responsible for inference. It is not training models. It does not own the GPUs [24]. It has effectively leveraged its existing power supply and transitioned into a highly specialized landlord.

Here are three of the disclosed contracts [11][12][24].

This gives us a defensible public-market range:

One megawatt of gross site power allocated to AI colocation can generate approximately $1.0–1.5 million of annual revenue, which is ~2-3x more than Bitcoin mining [11][12][24].

The contracts are usually quoted per megawatt of critical IT capacity, which excludes cooling and other facility overhead, while our Bitcoin figure uses total electrical input. Normalizing the disclosed contracts to gross site power lowers Core Scientific from $1.46M to approximately $1.04M per MW-year and TeraWulf from $1.85M to approximately $1.48M [11][12][24].

Even after normalizing the denominator, this topline comparison understates the economic difference between the two scenarios. With mining, the operating costs are higher given the miner has to also pay for electricity and refreshing ASIC servers [9][18]. In the colocation model, the contracts specify that electricity costs and capital expenditure are (partially) passed onto the tenant, with revenues contracted 10-15 years in advance [11][12][24]. Meanwhile, mining revenue is tethered to the price of Bitcoin, which could go up. Or down, on any given day [22].

Neoclouds

The neocloud model is far more ambitious, difficult, and financially lucrative. $IREN is currently the leading public Bitcoin miner pursuing this model at scale, where the miner purchases, maintains, and operates the GPU infrastructure itself [10]. This removes a significant pain point for the hyperscaler, whose focus now shifts to orchestrating the workloads running on top of the GPUs. More specifically, $IREN will spend approximately $5.8B purchasing GPUs and deploying them across four data centers representing 200MW of capacity [10]. In exchange, Microsoft will pay $IREN approximately $9.7B for dedicated access to that compute over an average five-year term [10].

We can construct a rough comparison by subtracting the cost of the GPUs from the contract’s topline revenue:

$9.7B of revenue − $5.8B of GPU capex = $3.9B of remaining spread [10].

Across 200MW and five years, that equals approximately $3.9 million per MW per year [10]. This is still not an apples-to-apples comparison, as $IREN’s remaining spread still needs to take into consideration electricity, data center construction, financing, networking, and expert staff to make all of this work [10].

But the rough #’s are still compelling:

Bitcoin Mining: $534K per MW [8][18][22]

Colocation: $1.0-1.5M per gross MW [11][12][24]

Neocloud, after GPU capex: $3.9M per MW [10]

Another fun fact. The next Bitcoin halving is in mid-2028, which will decrease the block subsidy from 3.125BTC to 1.5625BTC [22]. If the price of Bitcoin remains the same, revenue is cut in half. If the price of Bitcoin doubles, the revenue remains the same [22].

Offshoring

When I started working on this essay, I wanted to come to the conclusion that electricity was two to ten times cheaper in emerging markets. If miners could pay less than 1¢ per kWh in Paraguay or Ethiopia instead of 6¢ in Texas, offshoring would be a no-brainer. Unfortunately, this thesis was fundamentally wrong & the data does not support that argument. Publicly disclosed mining contracts generally cluster around 4–6¢ per kWh, suggesting a rough floor for industrial-scale power rather than some enormous geographic arbitrage [18][25][26].

The real advantage abroad is not necessarily cheaper electricity. It is less competition for the same electricity. A megawatt in Texas is increasingly contested by Bitcoin miners, hyperscalers, neoclouds, and enterprise data centers [27]. A megawatt of surplus hydroelectricity in Bhutan, Ethiopia, or Paraguay may have fewer comparable bidders [25][28]. Many enterprise AI workloads also carry latency, security, and data-sovereignty requirements that favor American infrastructure [29]. Bitcoin does not. The network treats a hash generated in Ethiopia exactly like one generated in Texas, and the resulting Bitcoin can be transferred anywhere in the world [1][21].

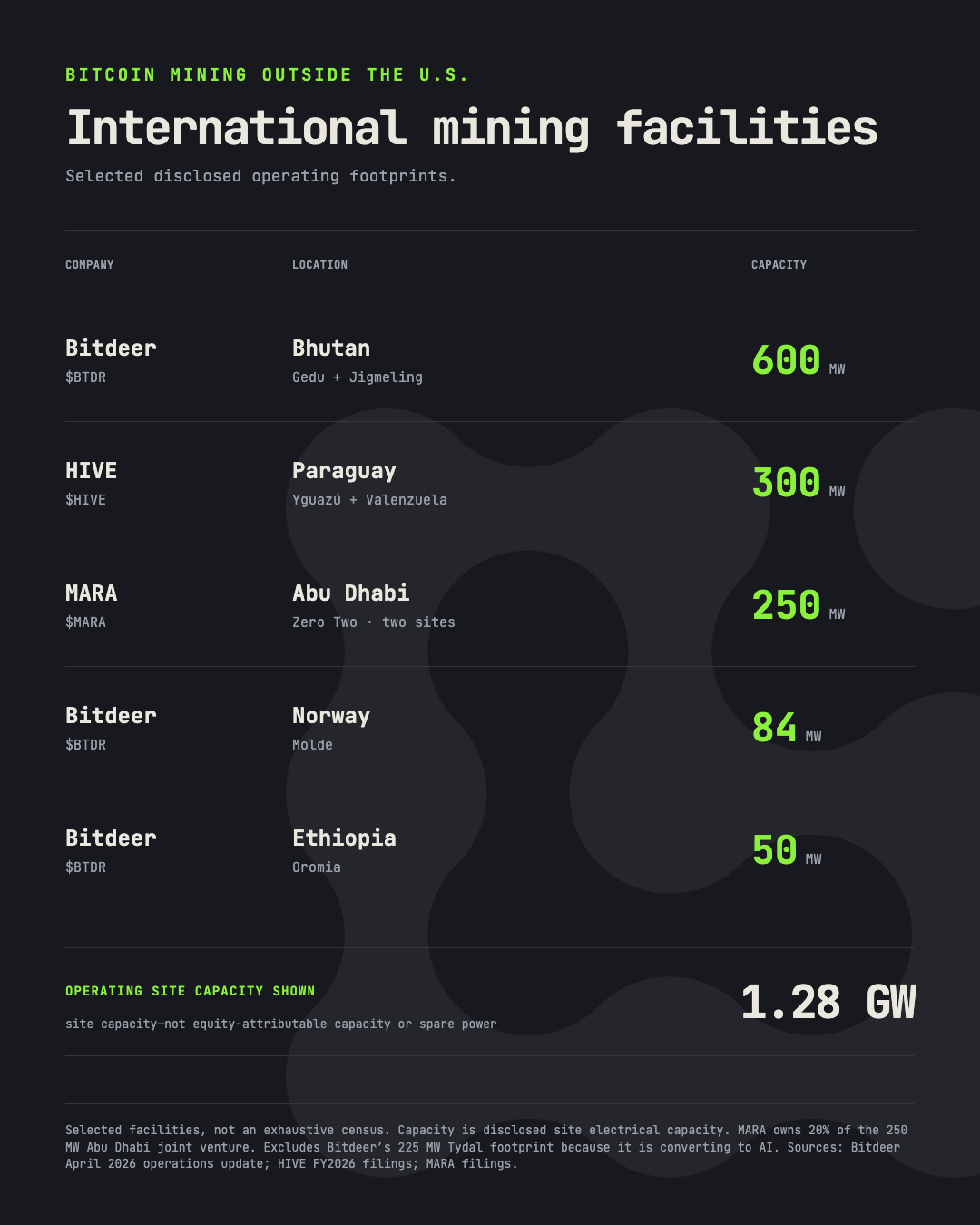

The international beachheads already exist. $BTDR, a Singapore-based company, operates 600MW in Bhutan and 50MW in Ethiopia [28]. $HIVE operates 300MW of hydro-powered mining capacity in Paraguay [25]. These are not empty facilities waiting to absorb America’s miners overnight. They are existing grid connections, operating teams, regulatory relationships, and import channels that give their owners a head start when the economics justify further expansion [25][28].

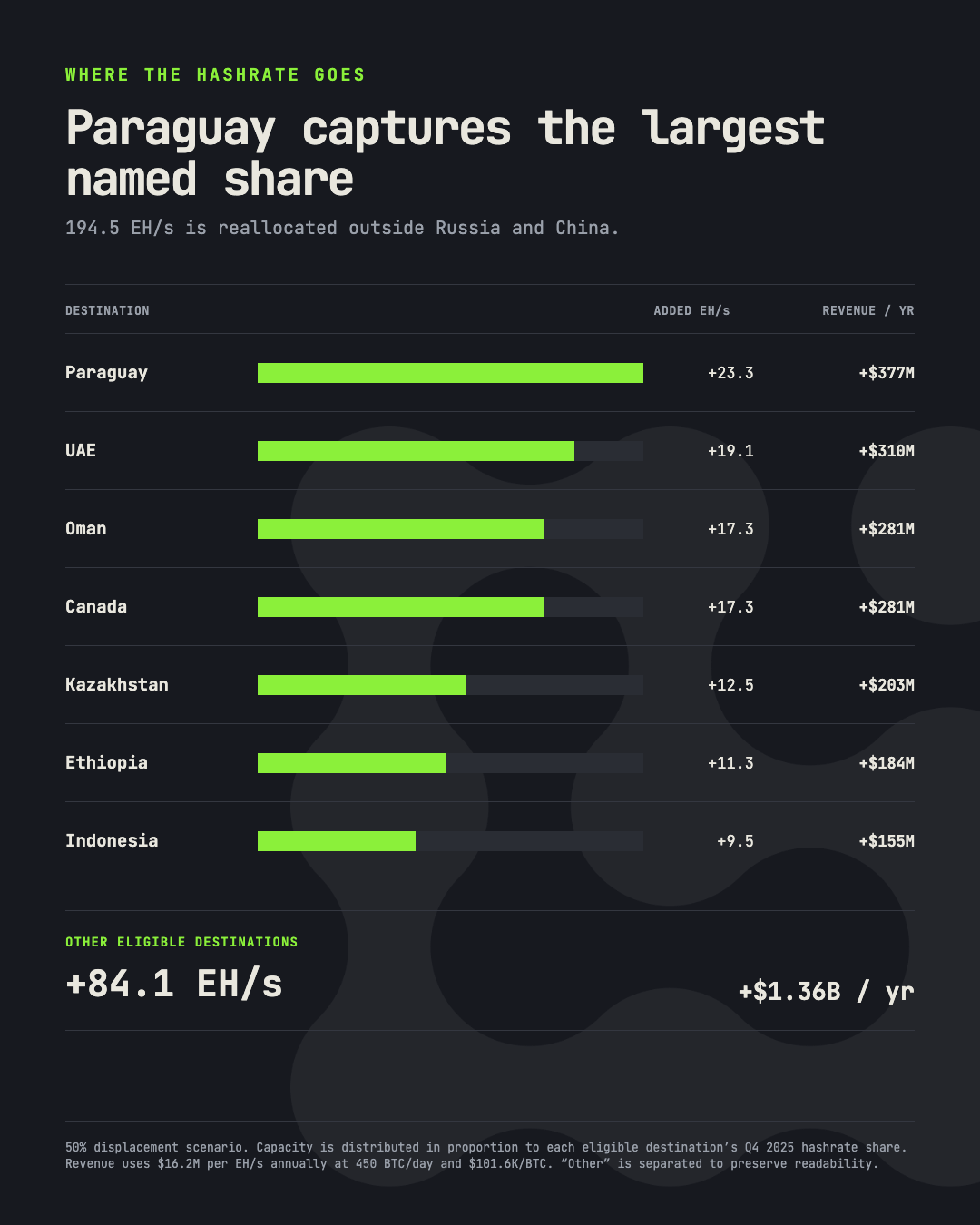

Today, the United States is estimated to control approximately 37.8% of global hashrate, or 389 EH/s [9]. We predict that AI will displace 50–75% of that capacity, creating approximately 195–292 EH/s of geographic rebalancing. In our default 50% scenario, 194.5 EH/s and approximately $1.99 billion of annual gross mining revenue are exposed to geographic reallocation away from the United States [8][9][22]. That does not mean all $1.99 billion automatically moves internationally. Once mining difficulty adjusts, the revenue is redistributed among the miners that remain online, wherever they are located [21].

Legislation solves everything

I hope the sarcasm in that title is obvious. Imagine the following headline appearing in 2028:

WASHINGTON — The Treasury Department today announced the first payments under the American Hashrate Security Act, establishing a minimum revenue guarantee for Bitcoin mined on American soil. “The infrastructure securing a strategic American asset cannot be allowed to migrate overseas,” the Energy Secretary said. Critics describe the program as a taxpayer-funded bailout for an industry that’s struggled to prove its utility to the average American household.

The American Hashrate Security Act does not exist. But the incentives that could produce it are beginning to form.

In March 2025, the United States established a Strategic Bitcoin Reserve [30]. That decision created a strange contradiction. The government declared Bitcoin strategically important [30] at the same time that markets began paying American miners to do something else. If AI continues absorbing the country’s data-center capacity, Washington may eventually discover that owning the asset and controlling the infrastructure underneath it are two different things.

We have seen the United States make the same mistake before. Semiconductor fabrication moved overseas because manufacturing was cheaper [31]. And then chips became strategically important and Congress passed the CHIPS Act [31]. Rare-earth processing had consolidated in China [32]. And then the Department of Defense began funding domestic production and guaranteeing minimum prices [33]. The government repeatedly allows markets to offshore critical infrastructure & then spends billions attempting to bring it back [31][33].

Bitcoin mining could follow the same playbook. A future subsidy might take the form of a production tax credit for domestically mined Bitcoin, subsidized power contracts, accelerated depreciation on American mining equipment, or a minimum hash price guaranteed by the government. Any of these policies would improve the economics of mining relative to AI without requiring the government to explicitly nationalize the industry.

Whether that would be good policy is an entirely different question. Subsidizing Bitcoin mining would divert scarce electricity from other uses, reward companies that willingly converted their facilities to AI, and force taxpayers to support an industry specifically designed to operate without government support. It would be an extraordinarily ironic conclusion to Bitcoin’s institutionalization.

References

[1] Satoshi Nakamoto, “Bitcoin: A Peer-to-Peer Electronic Cash System” — https://bitcoin.org/bitcoin.pdf

[2] Brian Armstrong, “How crypto enables economic freedom” — https://www.coinbase.com/en-ca/blog/how-crypto-enables-economic-freedom

[3] Coinbase Advanced, derivatives trading and leverage disclosures — https://www.coinbase.com/derivatives-trading

[4] Coinbase Q3 2025 Shareholder Letter — https://investor.coinbase.com/files/doc_financials/2025/q3/Q3-25-Shareholder-Letter.pdf

[5] CoinGecko, “CEX & DEX Trading Activity Report 2026” — https://www.coingecko.com/research/publications/cex-dex-trading-activity-report-2026

[6] CoinDesk, “Bitcoin hashrate posts first-quarter drop for first time in 6 years as miners pivot to AI” — https://www.coindesk.com/markets/2026/03/30/bitcoin-hashrate-posts-first-quarter-drop-for-first-time-in-6-years-as-miners-pivot-to-ai

[7] Mungerisms, “Charlie Munger’s 25 Cognitive Biases” — https://www.mungerisms.com/cognitive-biases

[8] Kraken, Bitcoin price page — https://www.kraken.com/prices/bitcoin

[9] CoinShares, “Bitcoin Mining Report — Q1 2026” — https://coinshares.com/no-en/insights/research-data/bitcoin-mining-report-q1-2026/

[10] IREN Q2 FY2026 Form 10-Q, Microsoft and Dell agreements — https://www.sec.gov/Archives/edgar/data/1878848/000187884826000015/iren-20251231.htm

[11] Hut 8, “Hut 8 Signs 15-Year, 245 MW AI Data Center Lease at River Bend Campus with Total Contract Value of $7.0 Billion” — https://canada.hut8.com/resources/press-releases/hut-8-signs-15-year-245-mw-ai-data-center-lease-at-river-bend-campus-with-total-contract-value-of-usd7-0-billion

[12] TeraWulf, “TeraWulf Signs 200+ MW, 10-Year AI Hosting Agreements with Fluidstack” — https://investors.terawulf.com/news-events/press-releases/detail/112/terawulf-signs-200-mw-10-year-ai-hosting-agreements-with-fluidstack

[13] Riot Platforms Q1 2026 results, SEC Exhibit 99.1 — https://www.sec.gov/Archives/edgar/data/1167419/000110465926052943/riot-20260430xex99d1.htm

[14] Cipher Mining, September 25, 2025 SEC Exhibit 99.1 — https://www.sec.gov/Archives/edgar/data/1819989/000095010325012168/dp234624_ex9901.htm

[15] U.S. Energy Information Administration, “Measuring electricity” — https://www.eia.gov/energyexplained/electricity/measuring-electricity.php

[16] U.S. Energy Information Administration, “Electricity use in homes” — https://www.eia.gov/energyexplained/use-of-energy/electricity-use-in-homes.php

[17] U.S. Energy Information Administration, “The United States operates the world’s largest nuclear power plant fleet” — https://www.eia.gov/todayinenergy/detail.php?id=65104

[18] Cambridge Centre for Alternative Finance, “Cambridge Digital Mining Industry Report” — https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/cambridge-digital-mining-industry-report/

[19] U.S. Energy Information Administration, Electric Power Monthly Table 5.6.A — https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=epmt_5_6_a

[20] Riot Platforms, Rockdale Facility — https://www.riotplatforms.com/bitcoin-mining/rockdale-2-navy/

[21] Bitcoin Developer Guide, “Mining” — https://developer.bitcoin.org/devguide/mining.html

[22] MARA Holdings 2024 Form 10-K — https://www.sec.gov/Archives/edgar/data/1507605/000150760525000003/mara-20241231.htm

[23] Bitdeer, “Bitdeer Launches SEALMINER A4 Series Bitcoin Mining Rigs” — https://ir.bitdeer.com/news-releases/news-release-details/bitdeer-launches-sealminer-a4-series-bitcoin-mining-rigs

[24] Core Scientific, June 4, 2024 Form 8-K Exhibit 99.1 — https://investors.corescientific.com/sec-filings/all-sec-filings/content/0001628280-24-026483/corzcoreweavehpc.htm

[25] HIVE Digital Technologies FY2026 Form 10-K — https://www.sec.gov/Archives/edgar/data/1720424/000106299326002973/form10k.htm

[26] Bitdeer Technologies Group 2025 Form 20-F — https://ir.bitdeer.com/static-files/9b19f847-0428-4661-b9d7-0e8e29e72ef7

[27] U.S. Energy Information Administration, “Data centers and cryptocurrency mining in Texas drive strong power demand growth” — https://www.eia.gov/todayinenergy/detail.php?id=63344

[28] Bitdeer, April 2026 Production and Operations Update — https://ir.bitdeer.com/news-releases/news-release-details/bitdeer-announces-april-2026-production-and-operations-update

[29] Microsoft Azure Architecture Center, “Multitenancy and Azure OpenAI” — https://learn.microsoft.com/en-us/azure/architecture/guide/multitenant/service/openai

[30] Executive Order 14233, “Establishment of the Strategic Bitcoin Reserve and United States Digital Asset Stockpile” — https://www.federalregister.gov/documents/2025/03/11/2025-03992/establishment-of-the-strategic-bitcoin-reserve-and-united-states-digital-asset-stockpile

[31] Congressional Research Service, “Frequently Asked Questions: CHIPS Act of 2022 Provisions and Implementation” — https://www.congress.gov/crs-product/R47523

[32] U.S. Department of Energy, “Rare Earth Permanent Magnets: Supply Chain Deep Dive Assessment” — https://www.energy.gov/sites/default/files/2024-12/Neodymium%20Magnets%20Supply%20Chain%20Report%20-%20Final%5B1%5D.pdf

[33] MP Materials, July 2025 Department of Defense transaction presentation, SEC Exhibit 99.2 — https://www.sec.gov/Archives/edgar/data/1801368/000119312525157310/d43796dex992.htm